Tips for Reducing Your Medical Bills

Last updated: February 22, 2023

Some of the below advice is "Know Before You Go", so I recommend giving this a read through even if you aren't currently battling any medical bills. A lot of what I learned, I wish I had known before getting seen by a doctor. Alas, I overestimated the generosity of my insurance and the American healthcare system. Let my hard-won battles be your gain. Please note: I attempted to keep this as factual as possible; any additional anecdotes relating to my personal experiences are set in italics.

The following guidance draws from several sources: various articles found by googling "how to negotiate/reduce medical bills" (all linked at the bottom of this post), Reddit's r/MedicalCoding forum, and my own experience dealing with one urgent care bill & two emergency room bills (hospital & physician billed separately) that totaled $1600, which I negotiated down to $0 in the 7 months following my visits. Special shoutout to a doctor friend of mine who told me to negotiate my bills in the first place, and my friend Scott for proofreading this piece.

Quick refresh of terminology: The deductible is what you are 100% responsible for paying. After you meet your deductible, insurance kicks in and will cover some percentage (typically 80%) and you cover the rest by paying out of pocket (OOP). Then once you hit your specified OOP maximum (if your insurance has one), insurance will begin covering 100% of expenses.

THE CONTEXT:

In late April 2022, I contracted Covid. In the first week of May, some unexpected long Covid symptoms cropped up that caused me a bit of concern, so I called my PCP's office and they recommended that I visit an urgent care clinic since it was after-hours on a Friday. I was scheduled to fly out to meet my best friend in Atlanta the following day, so I continued with my itinerary and had my friend drop me off at a local urgent care clinic after we got brunch.

At the urgent care clinic, the physician's assistant did a brief physical examination. After explaining my symptoms and getting a chest x-ray, I was told that I have infiltrate in my right lung, “which could indicate a pulmonary embolism" and that I should go to an emergency room in case of a life-threatening clot. Though my symptoms hadn't worsened over the past 24 hours, I figured “I have health insurance, better safe than sorry", so my friends dropped me off at a nearby hospital. I waited about an hour to get triaged (nurses at the registration desk ask for the reason of your visit and slot you into the queue based on how severe your symptoms are). When I was finally admitted, they administered a couple tests (CMP, HCG, d-dimer, EKG, chest ultrasound), all of which I passed with flying colors (the doctor said my labs were “pristine”), and I was discharged less than 5 hours later. Two weeks later, I received a $501 urgent care bill, $798 emergency room hospital bill, and $270 emergency room physician bill (mind you, those amounts were AFTER insurance paid 20%). Cue Google binge and lessons learned over 7 months of calling the three different billing departments.

BEFORE YOU'RE ADMITTED

Remind your healthcare provider (HCP) that you want in-network care. Unfortunately, the provider can’t always determine for you if they're in-network or not, even when you tell them what insurance you have. To find out yourself, go onto your insurance provider's website and find the healthcare practitioner via the "Find a Provider" directory. Not all providers at the same location/building will be in-network, and coverage can vary among departments (e.g. ophthalmology vs. OB-GYN at the same clinic).

Ask your doctor if all the recommended tests or procedures are medically necessary before you get them. Don't be afraid to question their necessity, as you may be billed by insurance for each one.

Ask the receptionist if it's cheaper to pay cash than to use your health insurance. This is known as the cash rate (aka uninsured or self-pay rate). Sometimes the cash rate is cheaper than the provider submitting a claim to your insurance–a win-win for both of you.

I didn't think my fees would be exorbitant because my urgent care was in-network. Wrong. My $500 out of pocket urgent care bill could've been much less if I chose the self-pay rate of $200 for a bundle of a physical exam and x-ray of one body part.

For more information on whether insured patients are allowed to pay the cash rate, check out Marshall Allen's newsletter about a patient who saved $2000 by paying cash for her medical tests.

Ask for a discount if you have time to shop around and leverage prices from other providers

Caveat: I myself didn't shop around, as I naively thought going to any in-network urgent care or emergency facility would save me enough money compared to going out of network without having to compare in-network providers.

If visiting a new provider, bring a copy of your most up-to-date medical record. You should be able to get a printout of your patient profile or download a PDF from your online account. If you've had any x-rays done, ask for a copy (older organizations may transfer the file and viewer program onto a CD).

DURING THE VISIT

Write down basic info about the care you receive and the doctors you see, whether in your phone or with paper & pencil. Write down any tests you receive and get the business card of the doctor/specialist who sees you. If you don't have immediate access to your phone, jot down notes right after you're discharged. Taking notes makes it easier to remember what treatment you receive and help you negotiate later. For example, "2:41pm: I was admitted and wrote ___ as reason for visit on the form. 3pm: Got XYZ test done. 3:30pm: Waited 30 minutes for results in my individual room, etc." Take a picture of any forms, and screenshot if on mobile.

I wish I had done a better job of documenting my visit, but I at least made sure to ask plenty of questions to understand which medical tests were being administered, and I have a record of those in my itemized statement as well as on my online patient profile.

Again, during the visit, question whether the tests or treatments you're receiving are medically necessary. Ask why you're getting it. If you got bloodwork or an x-ray done recently with another provider, the doctor should be able to grab those electronic records.

In my case, when the emergency room triage nurses plopped me into a wheelchair and wheeled me toward the x-ray room, I vehemently declined getting another chest x-ray, because I already got a chest x-ray at the urgent care facility. The urgent care and hospital were two different medical organizations but Electronic Medical Records (EMRs) exist for a reason right? If they really needed to see my x-rays, they could contact the urgent care facility down the road.

Some providers will have you pay in advance of your visit. Verify whether it's absolutely necessary to pay at that time. Others will require payment following your visit, while insurance is still processing your claim. Either way, request an invoice that shows the insurance processing your claim.

If you pay ahead of being seen by the provider, you might owe less than you paid.

This happened to me at the dentist; they refunded me $60 once my insurance claim was processed, 2 weeks after I went in to get my cavities filled. For the urgent care and emergency room, I received bills in the mail two weeks after my date of service.

AFTER THE VISIT

You should receive an Explanation of Benefits (EOB) from your insurance provider (not the hospital). Sometimes it takes 1-2 weeks and you'll get an email or letter from insurance. EOBs AREN'T BILLS. A billing statement and EOB aren't the same. You don't pay an EOB, it's like a receipt.

In my case, my insurance covered 20% of my urgent care and emergency room balances, so I was left with a whopper for patient responsibility.

If you don't receive an EOB from your insurance provider within 2-3 weeks after being discharged, request it from your insurance.

If a charge wasn't covered by your insurance, check the notes section of the EOB to understand why. You have a right to appeal it.

Depending on your insurance policy, there may be a time limit on appeals; your provider has a requirement to abide by these time limits regardless of their internal audit.

You can also ask your insurance company to request records and do an audit of the level of service billed. They may not do it, but you can ask.

You will also receive a "pay this amount" bill from the hospital/doctor. This is probably not going to be itemized. Call the billing department and ask for the ITEMIZED statement, so that you can check what you’re being charged for.

What to say when you call the billing department: "Hi, I'd like to request an itemized statement with HCPS/CPT codes."

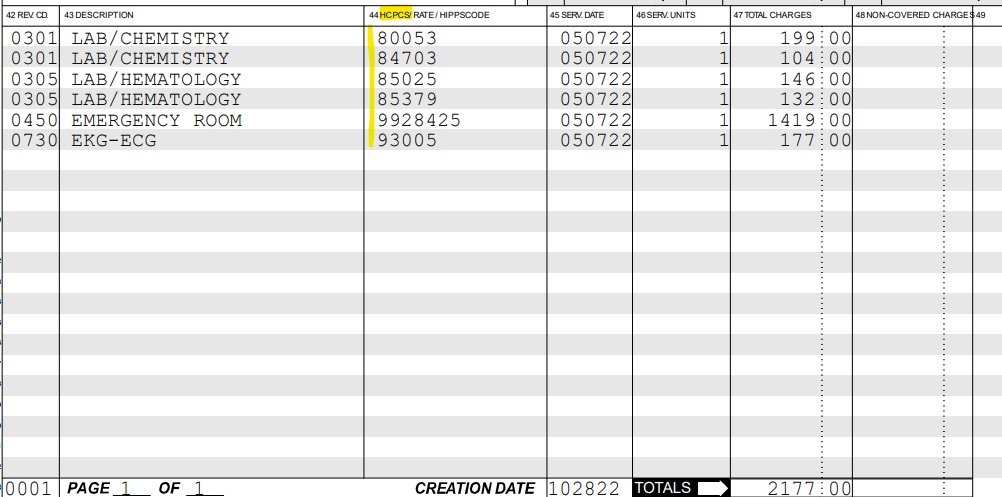

In my itemized emergency room bill, I noticed that I was charged for two EKG tests, even though one was performed.

The itemized statement of my emergency room hospital bill. I was charged for two EKGs despite only receiving one on my date of service. When I called the hospital billing department and pointed it out, my file was sent for review and the duplicate EKG was removed after 2-3 weeks. I also requested a correction of the Emergency Room coded 99285, because I did not agree that my visit was a Level 5.

Sometimes, the itemized statement isn't detailed enough and you need to call and request the UB04 claim form, which is the form that the provider sends to the insurance company. You should receive the itemized statement or UB04 via email or snail mail. Check it for errors — tests you don't remember receiving, incorrect provider names, duplicate medication/tests, charges for consultations. Make sure your name, address, and any other personally identifiable information is correct. Typos like that can result in an erroneously denied claim.

Check that the CPT (procedure codes) on your insurance's EOB match the provider's itemized statement. Check the billing and diagnosis codes (this will likely require some googling to decipher the definitions of the codes). Sometimes coverage might be denied based on codes submitted; maybe HCP used the wrong code or used a more severe code.

If it's an issue with insurance coverage, you can request a reconsideration or file an appeal

If it's a provider error, contact them immediately and ask that they review, recode, and resubmit the claim to the insurer.

Don't be afraid to call to ask what the bill and codes mean

Call the billing department and ask that the hospital audit the case to determine if it was coded correctly — "Hi, I would like to request my case to be sent for review by your coders because I have a question about ____." Document the time and content of the call.

If you received care in the emergency room, look to see what "level" of care you received. Hospitals "code" (verb) care in terms of severity; make sure it aligns with the actual care you received. You should be able to find the code level in your itemized statement and it should look something like 99282, 99283, 99284, 99285, or 99205. Ending in 5 is usually the highest severity.

If you look at my itemized statement above, you’ll see that my emergency room visit was coded as 99285-25. However, looking up the definitions of 99281-99285, my doctor friend and I agreed that my visit did not fulfill the criteria for a Level 5—“a comprehensive history, a comprehensive examination, and medical decision-making of high complexity”. At most, it was a Level 2 or 3, because medical decision-making was straightforward (“low complexity”) and my problem-focused history was short: I got Covid 2 weeks before the visit. After my duplicate EKG was removed, I requested a second review of my bill. Voila, a $85 pulse-ox test was removed and my emergency visit was changed from 99285 (Level 5) to 99284 (Level 4). I still believed it should be a Level 2 or 3, so I asked for a third review.

The highlighted column is the Current Procedural Terminology (CPT) code applied to each item of my visit. During the first bill audit, my duplicate EKG was removed (you see that there is only 1 count of it this time). During the second review, an $82 pulmonary function test was removed, and my visit was changed from 99285-25 to a 99284-25 (Level 4 with a -25 modifier). A doctor friend agreed that my visit was still up-coded in severity; my visit warranted a Level 2 or 3, not Level 4 or 5. This is something I disputed with the billing department a third time.

If you feel an acceptable level of care was not met (or if, like me, you are concerned with artificial up-coding of your visit), you can lodge a quality of care complaint. The provider's compliance hotline may be managed by a third party to avoid bias and retaliation.

The billing department might call you to request payment in the middle of your bill audit. However, payment isn't truly due until you receive a "Last Notice" in the mail, which is typically 6 months after your date of service.

In my case, I received service on May 07, 2022. Around August 2022, I got a call from the hospital billing department reminding me that my bill was due. They offered $100 off my $798 bill if I paid during that call. I declined (I admit I was a bit hesitant to pass up the discount), continued calling in about reviews of my bill through December, and now I owe $0.

Goodbill.com is a free service where you work with an individual case manager and medical coder to analyze your medical bills and see which items are worth negotiating or requesting an audit for. There are plans in the future to move to a business model where Goodbill receives a percentage of your bill savings, but at the time that I created my account, it was a free service.

My personal experience: Maybe it's because they're a startup and a free service, but I do not give them any credit in negotiating my 3 bills (two emergency and one urgent care) to $0. Instead, I relied on my Googling and advice from my doctor friend. When I wrapped up my bill negotiations in December 2022, my case had sat in the "In Review" stage on Goodbill for more than 2 weeks. I've subsequently requested a deletion of my account and all associated personal data, including uploaded medical records.

Contact the hospital’s compliance hotline if you're concerned that you were up-coded for the care you received

I did this for both the emergency room and urgent care. So one call to each organization's corresponding hotline.

If the reviews of your medical bills go well, two potential outcomes:

Coding errors and/or duplicate/incorrect tests are fixed, and insurance covers the medically necessary/correctly coded procedures. Your patient responsibility is severely reduced or zeroed out.

The provider may write off your reduced patient balance "as a gesture of good will" if they're tired of dealing with you. In my case, after I called to request a third review of my emergency hospital visit, because I believed my visit should've been a Level 3 (I stated, "I would like an explanation as to why my visit was coded as Level 4 instead of a Level 3, due to ____".) The billing rep said something along the lines of, "You're calling about your $231 that was reviewed twice? I'll write it off as a gesture of goodwill". El fin.

While on the phone with the billing department, some additional tips:

Document all in-person and phone conversations. That means recording the name of the person who picked up your call + date/time of conversation + what was discussed, word for word if you can type that fast. Being polite on the phone goes a long way (e.g. "take your time", "ok thanks", "yes I'll wait on hold")

Call all parties involved to proactively postpone bills, even if you're in the middle of negotiating:

Whoever's billing you (internal or third party)

Source of your bills (hospital or doctor)

Any charity care provider you're working with

Insurance company

Schedule an appointment with the billing office to review your bills, explain insurance benefits, and direct you to other resources to maximize insurance benefits.

In my case, the billing department said no appointment needed, just call back when I have questions.

If a provider is corporate, you have an option to file a complaint with either the insurance company, state medical board, state health services department, or your state dept of insurance, whichever agency is applicable

If you're verbally given a payment offer, make sure to get it in writing. Request email summaries of conversations to create a paper trail. A hospital may provide a $100 or 10% discount for paying right away and the offer may not be available the next time you call. However, know that if your bill is sent for review, any corrections made might be more than the discount they offer for paying as soon as possible.

If contacting bill & debt collectors, take notes of the people you speak to and what you owe. Debt collectors can be penalized for using unfair tactics (e.g. threats, calling at odd hours).

If after all case reviews and appeals, there's been no change in your outstanding balance, or you're ready to pay up (it took me calling periodically over 7 months and I'm aware that not everyone has that time or energy), try the following requests:

Ask to pay the negotiated rate (the rate that insurers pay)

Ask for a discount if you pay cash

Ask for a discount if you pay lump-sum

Ask for a discount if you pay over the phone (or online)

Ask if an interest-free payment plan is available: "I am willing to pay something, but am unable to pay the entire amount. Given my financial situation, what are the discounted payment options available for me?"

Ask if any of the following are available: charity care, bridge assistance, patient financial assistance programs

Whether you have to share financial information to receive financial assistance varies according to your provider. Sometimes only in-state residents are eligible for financial assistance.

If asked to provide financial statements, you may be able to choose whether to use a bank statement, prior year tax return, or current income to tell the story.

Ask to pay the Medicare rate (HCPs are familiar with this)

Ask if there's an ombudsman who can help review the quality and necessity of my care

Ask if any of the fees be paid via HAS or HRA (health reimbursement arrangement through employer)

Additional advice from Reddit:

"There is a legal argument that the utilization of the services is an open contract and that charges must be usual and customary if that is the case (Caveat - I am not an attorney and state laws differ so you would need to check). You should write them a letter - always put it in writing - and compare their charges to other data. For lab charges, you can usually find LabCorps' walk-in charges listed online - they will be substantially lower than what you were charged. For CT scan, look for local imaging centers that are privately owned for a comparison."

"I would also loop in your local consumer media reporter - they love stories like this and oftentimes the publicity will help you get a reasonable rate. Background: I’ve run billing operations for large ER groups and companies for the last 20 years and am pretty passionate about helping people fight these predatory practices."

Happy negotiating! Save your hard-earned money and spend it on ice cream, not $$$$ healthcare bills.

Resources (not sponsored)

The secret to negotiating lower medical bills | PeopleKeep

20 ways to save on medical bills | Investopedia

Don’t pay a medical bill until you do these 6 things | Human Health Advocates

How to best prepare yourself for negotiating medical bills | Healthcare Insider

6 things to remember as you negotiate medical bills | Healthcare Insider

Yes, you can negotiate your medical bills. Here’s how to lower your costs | CNBC