How to Open an Individual Retirement Account

Now that you’re armed with the knowledge from reading Personal Finance 101: 401(K) Plans and IRAs, let’s help you open an Individual Retirement Account.

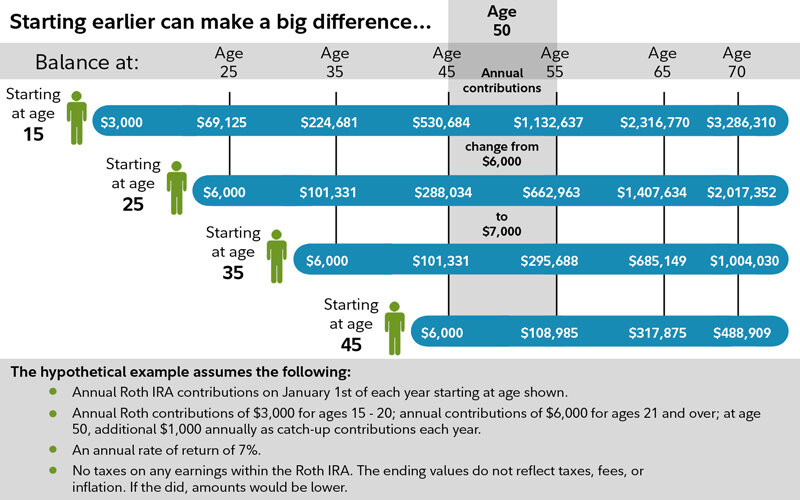

Photo by Fidelity Investments

ALRIGHT, WHAT DO I GOTTA DO?

First, pat yourself on the back taking control of your finances!

If you haven’t yet, head over to Schwab, Fidelity, or Vanguard to open a free Individual Retirement Account.

I get ZERO money for my referral link to Schwab, but you’ll get $100 bonus for the first $1k you deposit! Free money is a no brainer—you could view it as an easy-peasy no-stress-about-the-stock-market 10% return on your $1k.

Click “Get Started” or “Open an account”. You’re tech-savvy; you can find the account creation button—I believe in you.

Select “Roth IRA” or “Traditional IRA”. You can maintain both kinds of accounts, but you’ve gotta open one at a time.

What I do: I personally have only a Roth IRA, since I am over the $65,000 income limit to get a tax deduction for having a Traditional IRA. I predict that my income will grow, so I’d rather pay taxes on the money going in now (Roth) and let it grow so that I can have tax-free treatment on the money coming out when I withdraw it. Also, Roth IRAs don’t have Required Minimum Distributions at age 72 like Traditional IRAs do, so I could pass down my Roth IRA account to my spouse, kids, or charity if I wanted to. Plus, you can withdraw Roth IRA contributions (not earnings) at any time without penalty if you’re strapped for cash.

You’ll be asked for info about yourself—name, address, birth date, employer info, SSN.

Link your bank account info so you can deposit some money to start off before April 15. You might have to wait 1-5 days to verify the connection of your bank account, or it could be instantly verified.

Once your bank is linked and verified, schedule your first deposit of funds from your bank account into your IRA. Make sure you choose “2019” and not “2020”! You have the rest of 2020 to contribute to 2020, but until 2 more months until 2019’s contribution period ends.

The money may take 2-4 days to settle in your IRA.

Even though you’re opening the account in 2020, you’re eligible to contribute funds toward the 2019 $6,000 limit until April 15, 2020, so get to it! After April 15, 2020, you’ve got until next April—a full year—to work on contributing toward the 2020 $6,000 limit.

Buy some index funds or individual stocks with your newly deposited money. If you’d like to set it and forget it, any of the three online brokerages offer “smart portfolios”, where the funds are automatically rebalanced (i.e. you slowly hold more bonds) to become less risky as you get older. The only caveat is that you pay a small management fee (usually ~0.25% of your assets) because convenience costs money.

What I do: my Roth IRA is all index funds, aside from 4 shares of Apple (AAPL) that I purchased for fun at $142.

Individual stocks are a gamble and shouldn’t be your priority purchase. The majority of my account is in index funds because I know that the market will perform positively over the long run (I’m talking 20-30 years). Even if the market is dipping into a correction now, I am confident that the market will recover, just as it did after the 2008 recession.

If you want, you can worry about what to buy with your money later. It’s more important that you try to deposit as close to $6,000 as possible by April 15, because you can buy/sell stocks/ETFs/mutual funds any time after; there’s no deadline.

Roth vs Traditional IRA chart. **2020 EDIT: Required minimum distributions begin at 72. Photo by Fiscal Femme

Note: Before you bump up your retirement savings contributions, you should work to 1) eliminate any high-interest debt (e.g. credit card debt, student loans, car payments) and 2) have an emergency fund of 3-6 months’ worth of expenses kept in a high-yield savings acccount in case you’re ever laid off—enough to cover rent, phone bill, groceries, car, insurance—or have an unplanned medical emergency. I’ll explain the order of operations of saving money in a future post, but you should also contribute enough to your 401(K) to get your employer match before you start trying to max out your IRA limit.

Note: You can have an IRA open at more than one type of brokerage, but the max you can contribute to all accounts is $6,000 per tax year (April-April).

Note: Your credit score will not be pulled for opening an IRA.

ADDITIONAL RESOURCES I LOVE

Personal Capital ($20 for the both of us when you sign up using my referral link!)

Personal Capital is a free online tool that allows you to combine all your retirement, checking/savings, credit card accounts in one place so you can track your net worth (hopefully you’re positive, but I get that student loans are tough), analyze your portfolio for free and get recommendations on how to diversify it, and run a simulator that calculates how much money you should save for retirement based on how much you plan to spend per year & what age you plan to stop working. Your net worth updates every time you log in, and it’s fun to see the progress I’ve made over the past 2 years.

A solid place for more info about credit cards, banking, investing, loans, and general personal finance tips

Reddit’s Financial Independence / Retire Early Community

Reddit’s forums are pretty active, so it’s interesting hear what people are thinking re: current news and their investments. People in this sub-community are quite helpful when it comes to advice about maximizing your savings/wealth potential and tips to get there.